ICBA works closely with our affiliated state associations to identify creative ways to communicate our collective message to Congress and the regulatory agencies.

Aaron Stetter & Joe Schneider: ICBA state association partnerships

December 01, 2022 / By Dan Farmer

ICBA works closely with our affiliated state associations to identify creative ways to communicate our collective message to Congress and the regulatory agencies.

Advocacy is a group effort. It’s most effective when we all work together toward the common goal of creating and promoting an environment where community banks flourish.

That’s why ICBA partners with a network of 44 affiliated state associations throughout the year to engage lawmakers and regulatory agencies to address the challenges faced by community banks of all sizes and charter types.

“The partnership between the state associations and ICBA is instrumental for the industry’s continued success.”

—Colin Barrett, Tennessee Bankers Association

“ICBA has long been the community bank voice in Washington D.C., but just as we need their voice inside the Beltway, they need us carrying the message back home,” says Kraig Lounsberry, president of the Community Bankers Association of Illinois.

“As a state, we depend on the policy experts at ICBA to educate our bankers so that they can be effective in working with our congressional delegation,” says Colin Barrett, president and CEO of the Tennessee Bankers Association. “The partnership between the state associations and ICBA is instrumental for the industry’s continued success.”

What does that look like?

ICBA Capital Summit. Affiliated state groups helped facilitate more than 300 in-person or virtual meetings when the ICBA Capital Summit returned to Washington, D.C., last spring. This coordinated effort shows the size and influence of the community banking industry.

Pushing back against harmful credit card legislation. ICBA and its affiliates pushed back against the Credit Card Competition Act of 2022 (S. 4674), also known the Marshall-Durbin bill, warning Congress that the bill would undermine the safeguards that protect credit card payments—with consumers and community banks ultimately paying the price. The bill would overhaul credit card lending by creating new mandates requiring banks with more than $100 billion in total assets to enable their credit cards to be used on at least two unaffiliated networks, forcing a costly fundamental and, ultimately, unnecessary change to the system that community banks would have to subsidize.

ICBA reached out to Congress and issued a joint letter signed by all 44 ICBA-affiliated state associations to make the case for why this legislation is a bad idea.

Preserving consumer overdraft protection. ICBA and its state affiliates continue to oppose harmful overdraft legislation in the House and sent a joint letter to the House Financial Services Committee. The Overdraft Protection Act of 2022 (H.R. 4277) contains overdraft restrictions that would force many community banks to stop offering overdraft protection services to customers, consequently resulting in bounced checks, declined debit card transactions and credit rating harm, among other unintended consequences.

Standing together against credit union expansion. Credit unions have doggedly pursued expansion, including H.R. 2543, which passed the House earlier this year and would expand the fields of membership and commercial lending powers of tax-exempt credit unions without ensuring they serve low‑income individuals.

ICBA and its state affiliates sent a joint letter to Congress opposing this harmful expansion and are determined to prevent this legislation from getting a vote in the Senate.

ICBA has also worked closely with our affiliated state associations by sharing best practices that states have used successfully to address credit union acquisitions of taxpaying community banks. While ICBA doesn’t directly engage in state-level advocacy, we facilitate communication among the state associations to ensure ideas are shared.

Safe Banking Act. In another joint letter, ICBA and our affiliates continued to push for passage of the SAFE Banking Act in the Senate. The bill would create a safe harbor from federal sanctions for financial institutions that serve cannabis-related businesses (CRBs), as well as the numerous ancillary businesses that serve them, in states and other jurisdictions where cannabis is legal.

ICBA is working with the states for the bill to be taken up during the lame duck session.

Limiting the impact of climate-related risk management. With regulators discussing climate-related regulation, ICBA and its state partners reached out to the FDIC in a joint letter urging that any climate-related financial risk management principles for large banks do not trickle down to community banks and choke off lawful but climate-disfavored industries from the banking system.

Additionally, state associations work closely with ICBPAC to support pro-community bank candidates at the state level. ICBA also worked closely with the Florida Bankers Association to raise and disburse over $200,000 in funds raised through the ICBA Foundation Disaster Relief Program to help Florida community bankers and their families affected by Hurricane Ian.

Heading into 2023, ICBA will continue to work closely with our affiliated state associations, meeting monthly to identify creative ways to continue to communicate our collective message to Congress and the regulatory agencies. The fight is never over.

Dan Farmer

Subscribe now

Sign up for the Independent Banker newsletter to receive twice-monthly emails about new issues and must-read content you might have missed.

Sponsored Content

Featured Webinars

Join ICBA Community

Interested in discussing this and other topics? Network with and learn from your peers with the app designed for community bankers.

Related Articles

Do You Want to Be Featured in Out of Office?

CulturePeople

The Best Community Banks to Work For 2025

CulturePeople

How to Encourage Innovation Beyond the C-Suite

PeopleEducation and Training

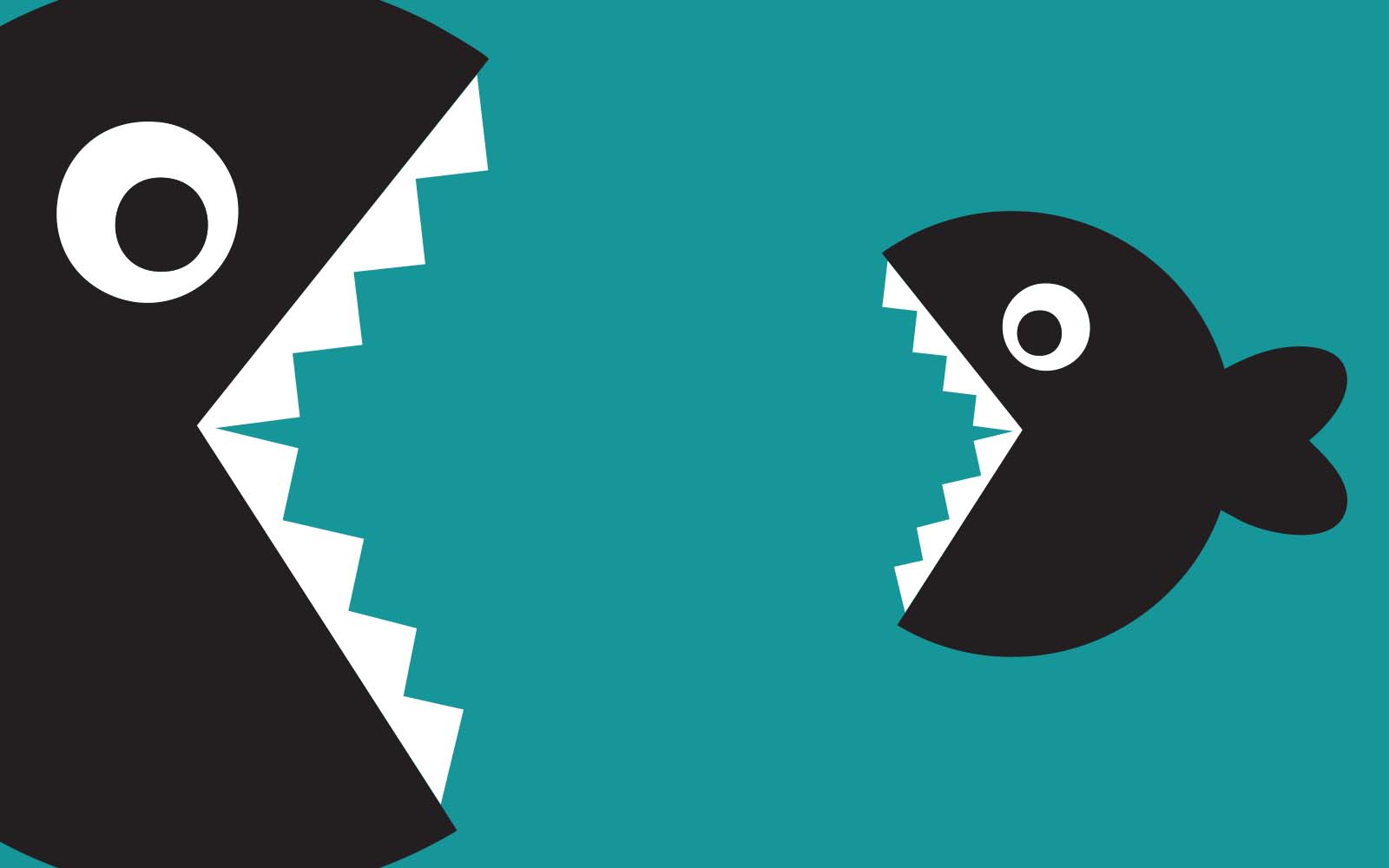

Revealed: The Impact of Credit Union Acquisitions

Grassroots ActionAdvocacy

Subscribe Today

Sign up for Independent Banker eNews to receive twice-monthly emails that alert you when a new issue drops and highlight must-read content you might have missed.

News Watch Today

Join the Conversation with ICBA Community

ICBA Community is an online platform led by community bankers to foster connections, collaborations, and discussions on industry news, best practices, and regulations, while promoting networking, mentorship, and member feedback to guide future initiatives.

Join the Community Example Text