The ripple effects of the Great Recession on the de novo market have been far‑reaching. Now, the pandemic is making more waves for young banks.

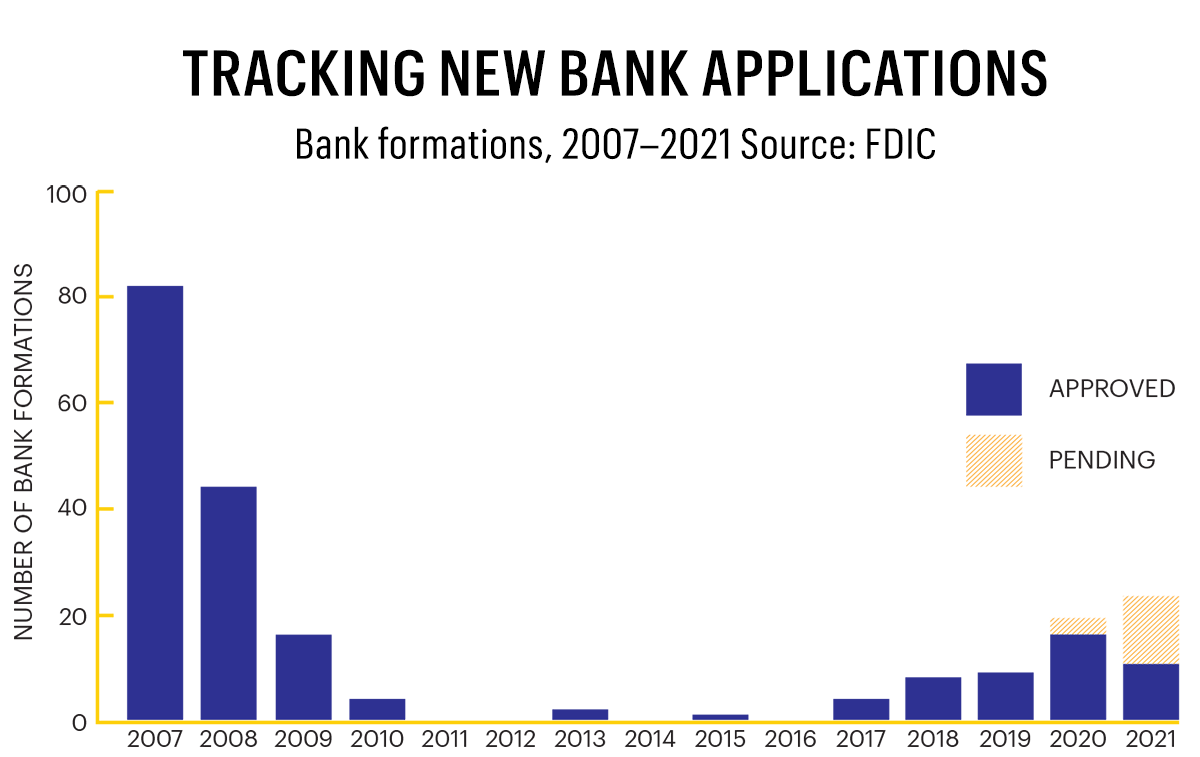

Chris Cole, executive vice president and senior regulatory counsel for ICBA, says the numbers tell the story. As of mid-November, there were 16 pending new deposit insurance applications with the FDIC. Of those pending applications, only 11 were applications for traditional bank charters. Before the Great Recession, 50 to 100 traditional bank applications would typically have been under consideration.

Cole believes the lower application rates can be attributed to the difficult environment that bank startups face. He notes that low interest rates mean tight margins, a problem compounded by depressed demand for commercial lending.

“We still aren’t seeing anything near the kind of de novo growth you saw before the Great Recession of 2008,” Cole says. “But you are seeing a little uptick in activity from the summer, and that’s a good sign.”

New banks are getting creative to flourish. Lori Maley, CEO and president of Bank of Bird-in-Hand in Bird-in-Hand, Pa., says when her community bank got its charter in 2013, no one was certain that the items in the original business plan and FDIC de novo order would be completed with ease.

“Then we blew our business plan away,” she says. “We opened the doors and literally they came, and they kept on coming.”

For the $700 million-asset bank, success came from understanding the Amish and Mennonite communities that it serves. At its flagship branch, Bank of Bird-in-Hand erected a barn so customers could leave their horses and buggies and safely conduct business. The community bank also converted three RVs, popularly known as the Gelt buses—“gelt” is Pennsylvania Dutch for money—into mobile branches. Ranging from 29 to 39 feet in length, the mobile branches travel to 16 locations in Lancaster and Chester counties, allowing customers who don’t drive motor vehicles to communicate with a banker face to face.

Bank of Bird-in-Hand employees with one of their Gelt buses, mobile branches that travel to 16 locations.

Opening in a pandemic

Pandemic-era de novos are facing down other challenges. “I never thought I’d be launching a bank from home,” says Stephen Gordon, the founding chairman and CEO of Genesis Bank in Newport Beach, Calif. But while the de novos of 2021 certainly started under unusual working conditions, the greatest stumbling blocks came not from Zoom meetings or even regulatory demands. What has been most daunting for the latest crop of de novos is the business environment.

“Folks that we thought would be investors did not invest, because they said that the impact of the pandemic on their businesses was unclear,” says president and CEO Mike Ives of Integrity Bank for Business, which opened for business in May 2021. He adds that the bank’s region of Virginia Beach, Va., relies on the tourism industry, and the hospitality sector was especially hard hit.

That said, young banks already in operation during the pandemic benefited from the Paycheck Protection Program (PPP).

“A lot of small businesses that were having trouble getting PPP loans from the big banks and regional banks went to the smaller ones,” Cole says. “Many of the de novos got a lot of new customers through the PPP.”

Pictured, from left: deputy chief credit officer Peter Reeves; chief operating and lending officer Leigh Keogh; assistant chief deposit officer Maureen Grover; president and CEO Michael Ives; chief deposit officer Melonie Whitehead; and chief development officer Neal Crawford.

Paths to starting a de novo

Bankers contemplating a new venture typically weigh applying for a de novo against acquiring an existing charter. Since the pandemic, the scales have arguably tipped in favor of acquisitions, according to Greyson Tuck, an attorney and consultant at Gerrish Smith Tuck Consultants and Attorneys, PC in Memphis, Tenn.

The pandemic lowered the market value of existing banks looking to sell and spurred some previously undecided banks to make an exit, Tuck says. He notes that the stock of affordable bank charters is making it more attractive for buyers to make an acquisition. Many acquired banks are profitable on day one, while it typically takes de novos two or three years to achieve profitability, he adds.

Another sticking point for de novos is raising enough capital to secure regulatory approvals.

Capital requirements for de novos are generally twice the levels prior to the Great Recession, according to FDIC data. Since 2015, the average capital requirement for de novos has been approximately $34 million.

First Bank of Central Ohio CEO John Smiley

These capital thresholds are not an impossibly high bar. In 2021, First Bank of Central Ohio raised $28 million in six weeks by targeting businesses in real estate and the medical and dental sectors. “We could have raised more, but for us there’s a point where too much capital isn’t good. You can’t get it to work fast enough,” says CEO John Smiley.

Smiley believes the de novo route has distinct advantages over acquiring a bank charter, especially with acquisition opportunities as scarce as they are in Columbus, Ohio. “There’s a need, because so many banks have gone by the wayside,” he adds.

While Smiley says acquisition may be a faster route, it took only about a year for First Bank of Central Ohio to open, which it did in April 2021. By taking the path it did, the bank was “able to start something fresh,” he adds.

Signing on customers is yet another hurdle for de novos. “You’re having to take market share away from other banks to get customers, unless you’re in a really high growth area,” Cole says.

Tuck agrees. “De novos may have customer relationships with individuals, but they don’t have longstanding, deep-rooted, ‘I’ve banked at this bank for 20 or 30 years,’ types of relationships,” he says.

Finding your niche

One solution is to target a specific niche, a strategy used by Bank of Bird-in-Hand. Maley says understanding the Amish community’s commitment to helping one another is how Bank of Bird-in-Hand is growing $100 million to $150 million in assets each year while successfully raising capital, too. “The people we serve will repay their loans,” she says. “They’ll eat turnips if they have to, but they’ll pay you back.”

Several new banks, such as Genesis Bank, are targeting a digitally savvy niche. “The pandemic forced everybody of every age and every demographic to change their behavior and embrace technology,” Gordon says. “Everyone learned how to transfer money, pay bills and wire funds either online or through mobile.”

Genesis Bank has no legacy systems or platforms. “We have our fingerprints all over the technology,” he says. “We’re able to entirely focus on the client in the manner that the client wants to function.”

Regardless of niche, it’s important for any de novo or community bank to understand its target customer and how to address their needs. “In the end, it’s the community that matters,” Maley says, “and we’re part of a community of people helping people.”

How one de novo reflects its diverse community

Genesis Bank in Newport Beach, Calif., is one of just two of the nation’s 143 MDIs, or minority depositary institutions, with the distinction of being diverse and multiracial, according to founding chairman and CEO Stephen Gordon. The de novo, which serves a “majority-minority” community in the Los Angeles area, also has a majority-minority seven-person board.

Gordon and the Genesis Bank team were inspired to launch the de novo, in part, because large banks pulled away from their communities during the pandemic. “There were many, many businesses left behind, and the banks did not step up and lead to the level that they should have,” he says. “We are putting our money where our mouth is by being designated an MDI.”

So far, the strategy is working. Genesis Bank opened in August 2021 with $57 million in capital, roughly half of which Gordon supplied himself. The bank is contemplating a second round of capital raising. “Being an MDI, there’s a very strong affinity for the institution and our mission,” Gordon says. “We’re drinking a little bit from a fire hose, and that’s a nice position to be in.”