Positive reviews from customers can make a community banker’s day. At one bank we spoke to, whenever feedback data shows a customer has been wowed by a product or service, the managers celebrate the employee who elicited the wow, include the customer in the celebration, and reward the employee with a small gift.

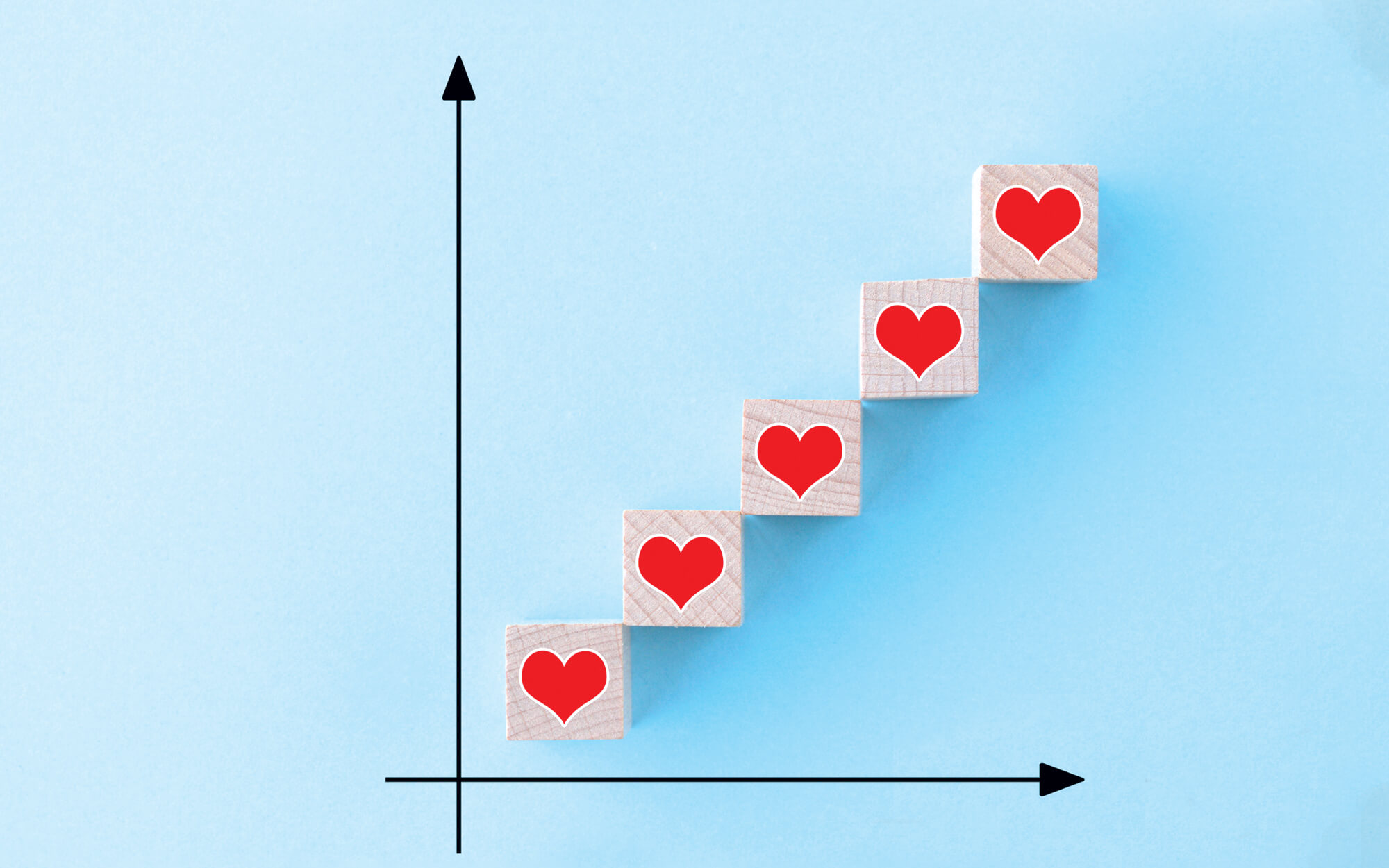

Quick Stat

1

The number of times per year customers want to provide feedback to banks

Source: Avannis

Emily Sayer, national sales director for Denver-based Avannis, which works with that community bank, regularly provides tools to financial institutions for measuring customer satisfaction. While data is key to getting granular with feedback, she believes that “flat” core data is more powerful when it’s supplemented by “listening to the customer voice.”

Community banks have myriad opportunities to parse all sorts of customer data, and yet many have shied away from using the data they possess. Rob Birgfeld, ICBA’s executive vice president and chief marketing officer, believes it’s because they associate know-your-customer (KYC) mandates with compliance rather than opportunity. He urges community bankers to pivot from merely collecting customer data to satisfy regulators to exploring what they can do with that data.

Here are six ideas for using customer data to boost your brand and turn your best customers into advocates for your community bank.

1. Start small

If a community bank is drowning in data, it should start by selecting a concrete project, such as determining when certain devices or channels are in use, Birgfeld advises. Knowing what times of day banking interactions take place can help banks more precisely time marketing messages, he says.

2. Take the customer pulse

Avannis periodically checks in with customers to “see how they’re feeling overall,” Sayer says. She notes that banks and their vendors can take the customer pulse in any number of ways, such as through online surveys, paper outreach, text messages and phone calls.

3. Mix and match data types

Gina Bleedorn, chief experience officer at branding firm Adrenaline in Atlanta, notes that internal customer data becomes more actionable when it’s buttressed by external data sources. Market data from the Census Bureau and services like Esri, which uses Geographic Information System (GIS) mapping, are two examples.

Another is competitor data, which Bleedorn notes is plentiful, thanks to the FDIC and other regulatory reporting. A third type of information is mobility data, which is aggregated and anonymized from cell phone records.

4. Begin exploring MAIDs

Cell phones are tracking “where people go, who they are and what they do,” Bleedorn says. She notes that mobile data can even be used to identify in-branch behavior. Taking this one step further, marketers have begun to use mobile advertising identifiers (MAIDs), which make it possible to send ads and offers directly to an individual’s device through proximity marketing.

By connecting a MAID with a customer record, community banks can augment account information with information on an individual’s daily habits, whether it’s how much time they spend driving a car or what time they typically walk by one of your bank’s branches.

This type of cutting-edge technology, Bleedorn concludes, is yielding “a new and priceless form of information.”

5. Pinpoint prompting events

“Marketing often sees its job as bringing folks in, not having the folks who are already here tell their story,” Birgfeld says. “It’s always better when the author [of a marketing sentiment] is the satisfied customer.”

Birgfeld urges bankers to identify “points of excitement,” or moments when customers are most likely to take the time and effort to share their experiences with a broader audience.

6. Make it easy to spread the word

“I’m a big believer in creating opportunities for your customers to tell your story on your behalf,” Birgfeld adds. He advises community banks to introduce prompts so customers can easily post about a positive experience on social media sites like Twitter, Facebook or Yelp. (For more on reviews, read “How to collect positive customer reviews”)

Turning a bank’s best customers into advocates is a numbers game. Birgfeld says that if one or two of every 100 people who are really excited about a product “share on social media or elsewhere because of a prompt on social media—or even if an individual texts a friend—that’s the most authentic marketing that you can possibly get.”

When should you solicit feedback—and when shouldn’t you?

Requesting customer feedback too often can alienate the very individuals you’re hoping to delight.

Avannis conducts an annual survey asking how frequently consumers want to give airlines, retailers and banks feedback about their services. According to sales director Emily Sayer, the average consumer wishes to give airlines feedback once every 3.8 years, retailers once every 3.1 years and banks annually. She says that six months is the point of oversaturation for banks, and so her company never reaches out to an individual banking customer more than twice a year.

While asking for feedback too often can be a no-no, so is failing to ask at all. “It would be very fair to say that when customers of a community bank are not asked [for feedback], they’re wondering why the heck their bank doesn’t care about them,” Sayer says. “Every other business is asking, so why would the bank, which has their money, not ask, too?”